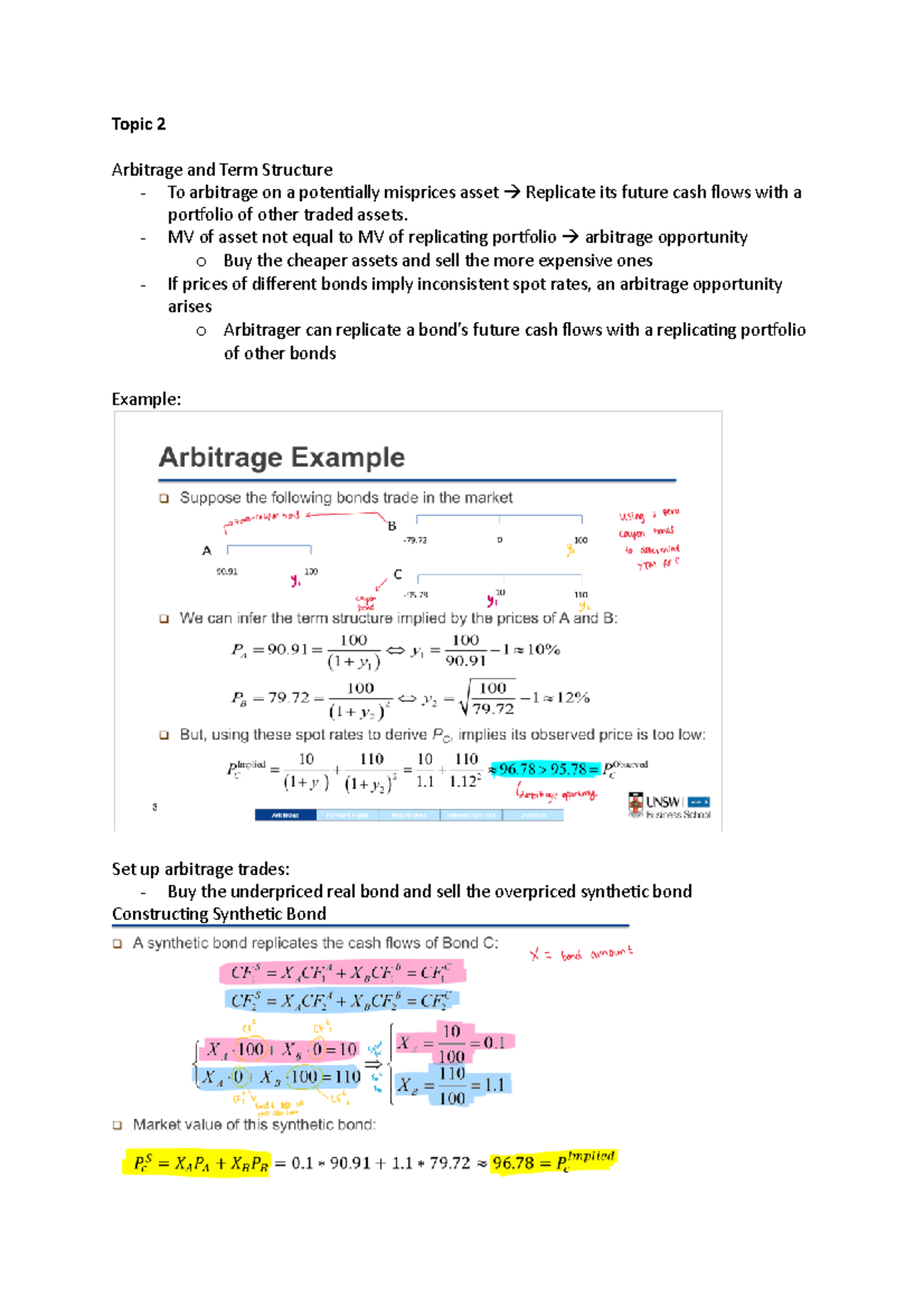

Capital preservation during exponential price appreciation requires a shift from valuation-based analysis to liquidity-driven risk management. When an asset enters a "parabolic" phase—defined here as a period where the rate of price increase exceeds the rate of change in fundamental value by several orders of magnitude—the traditional metrics of Price-to-Earnings (P/E) or Discounted Cash Flow (DCH) models lose their predictive power. Instead, the market enters a reflexive feedback loop where price action itself becomes the primary catalyst for further buying, creating a fragile structure prone to instantaneous collapse.

Michael Burry’s public stance on reducing positions "almost entirely" during such phases is not merely a contrarian whim; it is a recognition of the Asymmetric Risk-Reward Profiles inherent in late-stage momentum. The objective of this analysis is to quantify the mechanics of these blow-off tops and provide a structural framework for exiting positions before the liquidity window closes.

The Triad of Parabolic Fragility

To understand why a total reduction in position is a rational response to parabolic growth, one must categorize the three structural weaknesses that emerge during these cycles.

1. The Exhaustion of Marginal Buyers

Market price is determined by the last participant willing to pay the highest price. In a parabolic move, the pool of "sidelined" capital shrinks rapidly. As retail participation hits saturation and institutional "FOMO" (Fear Of Missing Out) peaks, the supply of fresh capital required to maintain the vertical trajectory disappears. When the number of new buyers falls below the number of profit-takers, the price does not merely plateau; it drops violently because the buy-side order book is thin.

2. The Reflexivity Trap

George Soros popularized the theory of reflexivity, which posits that investors’ biases and actions change the fundamentals they are observing. In a parabolic stock, the rising price improves the company's perceived creditworthiness and lowers its cost of capital, which in turn "justifies" a higher stock price. This creates a circular logic. Once the price stalls, this entire logic reverses: the perceived safety of the asset vanishes, margin calls are triggered, and forced selling begins.

3. The Liquidity Vacuum

During the ascent, liquidity appears infinite. However, this is "illusory liquidity." In a parabolic collapse, the spread between the bid and the ask widens significantly. If an investor holds a large position, they cannot exit at the "ticker price" because their own selling pressure collapses the market. Burry’s directive to reduce positions "almost entirely" acknowledges that in a crash, the exit door is too small for the crowd.

Quantifying the Parabolic Threshold

Vague descriptors like "overextended" are insufficient for professional risk management. A parabolic move can be identified by the Acceleration Gradient. If the second derivative of the price function is positive and increasing ($f''(x) > 0$), the asset is in a state of acceleration.

The danger zone begins when the Price-to-Sales (P/S) Z-Score moves three standard deviations above its five-year mean. At this juncture, the asset is no longer trading on expectations of future cash flows but on the expectation of a "Greater Fool" to buy the position later.

Structural indicators of a peak include:

- Volume Diminishment on New Highs: Price makes a new peak, but trading volume is lower than the previous peak, signaling a lack of conviction.

- Gap-Up Exhaustion: The asset opens significantly higher than the previous day's close multiple times in a week, indicating desperate entry by late-comers.

- Margin Debt Correlation: A tight correlation between the asset's rise and an increase in broker margin debt suggests the move is fueled by leverage rather than equity.

The Cost Function of the "Hold" Strategy

Most investors fail to exit because they focus on the Opportunity Cost of Exiting Early. They fear missing the final 20% of the move. A data-driven approach focuses instead on the Capital Impairment Risk.

If an asset has increased 500% and then drops 50%, a buyer at the peak requires a 100% gain just to break even. For a large-scale manager, the "cost" of staying in a parabolic trade is the potential loss of several years' worth of alpha in a single week of mean reversion. Burry’s strategy prioritizes the preservation of the "Principal + Unrealized Gains" over the speculative capture of the "Terminal Spike."

Structural Limitations of Diversification in Crises

A common misconception is that a diversified portfolio protects against a parabolic collapse in a specific sector (e.g., Tech in 2000, Housing in 2008, Crypto in 2021). However, high-momentum assets often have high Cross-Asset Correlation during a liquidity event.

When the largest "winners" in a market begin to fail, they trigger a cascade:

- Margin Calls: Investors are forced to sell their good assets to cover losses in their parabolic assets.

- Psychological Contagion: The collapse of a "market darling" creates a general risk-off sentiment.

- ETF Rebalancing: As the market cap of the parabolic stock shrinks, passive funds must sell shares, creating a feedback loop of downward pressure.

This proves that "reducing positions almost entirely" in the specific overextended asset is more effective than attempting to hedge with other correlated instruments.

The Execution Framework for Position Reduction

A disciplined exit does not require timing the exact top. It requires a systematic de-risking process based on the following milestones.

Phase A: The 2-Sigma Trim

When the asset price exceeds two standard deviations from its 200-day moving average, 25% of the position should be liquidated. This "takes the house money off the table" and lowers the psychological barrier to further selling.

Phase B: The Trend-Line Breach

Parabolic moves rely on a steep ascending trend line. The first daily close below this trend line, especially on high volume, serves as the signal to liquidate an additional 50%. This is the "Confirmation of Trend Change."

Phase C: The Residual Exit

The remaining 25% is held only as long as the short-term (e.g., 10-day) moving average remains upward-sloping. Once this flattens, the position is closed entirely.

Psychologically Anchoring to the Mean

The primary obstacle to following this data-driven strategy is "Anchoring Bias." Investors anchor their perception of the asset's value to its recent peak. If a stock hits $500 and drops to $450, they view it as "cheap" or a "buying opportunity," ignoring that the fundamental value might still be $150.

To counteract this, an analyst must look at the Mean Reversion Target. Historically, parabolic moves return to the "Point of Origin"—the price level where the vertical acceleration first began. If the Point of Origin is 70% below current prices, the risk of a "hold" strategy is mathematically untenable.

The Strategic Play: Capital Rotation into Asymmetric Value

Reducing a parabolic position creates a significant cash hoard. The strategic error most investors make is immediately seeking a similar "high-growth" replacement. In a post-parabolic environment, the broader market often undergoes a volatility expansion.

The optimal move is a transition into Defensive Value or Uncorrelated Assets. This involves identifying sectors with:

- Low Relative Volatility: Assets that ignored the parabolic move.

- High Replacement Value: Companies trading below the cost of their physical assets.

- Negative Correlation to the High-Flyer: Instruments that benefit from a "flight to safety."

The shift from a parabolic asset to a value-oriented one is not just a change in ticker symbols; it is a shift from Growth Gamma (betting on the speed of price) to Yield and Margin of Safety (betting on the floor of price).

Total liquidation of parabolic positions is the only way to ensure that the gains generated by market mania are converted into permanent capital. The market provides a window of extreme liquidity during the ascent; the disciplined strategist uses that window to exit before the crowd realizes the window has become a wall. Once the acceleration stops, the physics of the market dictate a rapid descent to the mean, and no amount of "belief" can override the mechanics of a liquidity vacuum.

Identify the current "momentum leaders" in the portfolio. Map their 50-day and 200-day moving average deviations. If the current price-to-moving-average ratio is at a multi-year high, execute a 50% liquidation immediately, regardless of news sentiment or projected earnings. Cash is the only asset that maintains its optionality when a parabolic cycle terminates.