The global race for artificial intelligence supremacy is fundamentally constrained by physical geology. While capital markets valuation models focus almost exclusively on algorithmic efficiency, compute parameters, and generative capabilities, the structural bottleneck of advanced technology lies in the midstream processing of critical minerals. Artificial intelligence infrastructure requires a material foundation that is currently governed by highly concentrated supply chains. Without control over specific physical inputs, software sovereignty becomes mathematically and logistically impossible.

To evaluate this exposure, the structural realities of the critical mineral market must be mapped against the hardware architecture required to sustain computational expansion.

The Material Infrastructure of Advanced Computing

The artificial intelligence hardware stack is heavily dependent on specific metalloids and rare earth elements (REEs) that serve specialized functions within semiconductors and data center infrastructure. The performance metrics of high-end graphics processing units (GPUs) and application-specific integrated circuits (ASICs) are dictated by atomic-level properties.

The Semiconductor Input Layer

High-frequency switching environments and high-performance logic chips depend on specialized mineral inputs:

- Gallium: Essential for gallium nitride (GaN) and gallium arsenide (GaAs) semiconductors, which manage power conversion efficiencies in high-voltage data environments. China currently commands 98 percent of global primary low-purity gallium production.

- Germanium: Utilized in fiber-optic communications, infrared optics, and high-speed polymerization. China controls over 60 percent of global germanium refining capacity.

- Indium and Tantalum: Used for transparent conductive layers and high-reliability capacitors in extreme thermal environments.

The Energy and Thermal Management Matrix

Data centers scale along an energy consumption function. The physical hardware supporting this power loop includes:

- Copper: The primary vector for electrical transmission and high-density thermal heat sinks. A typical modern AI data center requires significantly higher copper intensity per megawatt than traditional enterprise cloud facilities due to the thermal dissipation needs of densely packed server racks.

- Rare Earth Elements (REEs): Elements such as neodymium, praseodymium, and dysprosium are required to produce the permanent magnets found in high-efficiency cooling pumps and hard disk drive actuators. China dictates approximately 70 percent of global extraction and nearly 90 percent of global processing for these 30 key REEs.

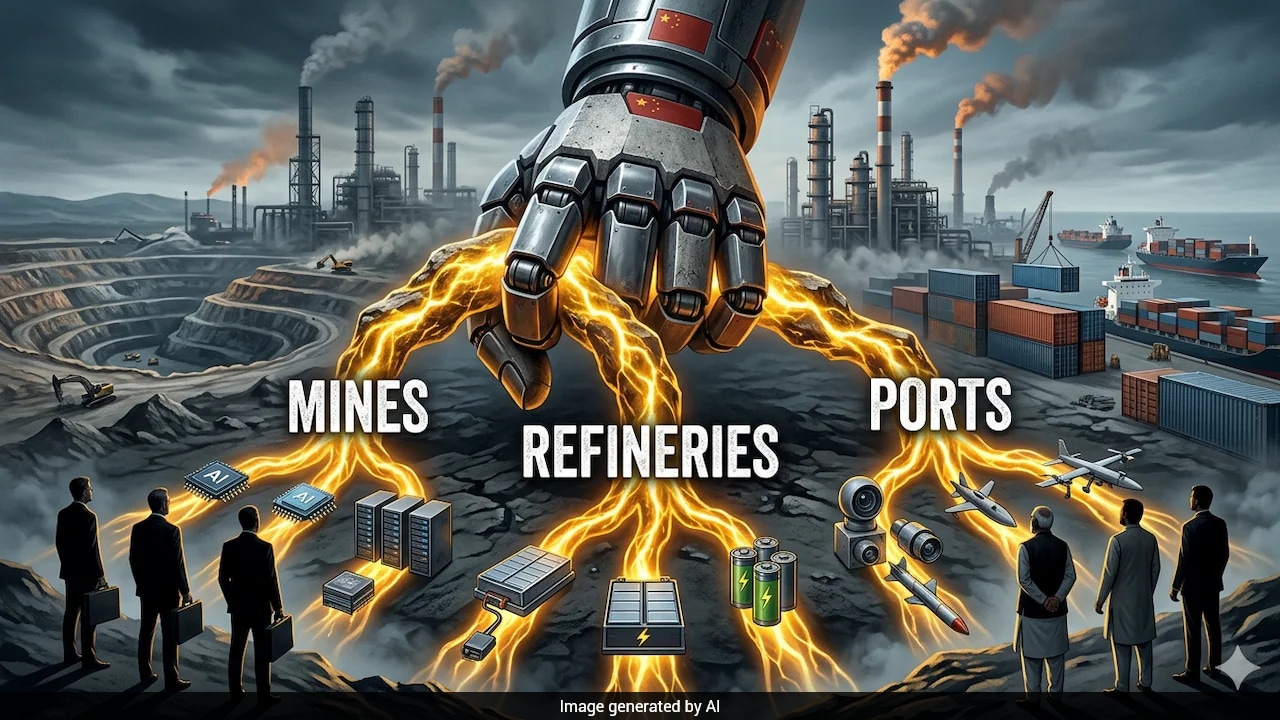

The Mechanics of Structural Dominance

The asymmetrical leverage held by Chinese state-supported enterprises is not merely a consequence of domestic geological deposits. It is the output of a long-term economic model engineered across three distinct structural pillars.

+-----------------------------------------------------------------------+

| THE THREE PILLARS OF MINERAL DOMINANCE |

+-----------------------------------------------------------------------+

| 1. BYPRODUCT CAPTURE |

| Extracting critical minerals as low-cost structural externalities |

| of massive industrial operations (e.g., Aluminum Smelting). |

+-----------------------------------------------------------------------+

| 2. MIDSTREAM PROCESSING MONOPOLY |

| Accepting localized environmental degradation and capital intensity|

| to control the refining phase where value is unlocked. |

+-----------------------------------------------------------------------+

| 3. PREVENTATIVE OFFSHORE ASSET ACQUISITION |

| Outbidding Western private equity with state-backed premiums |

| to secure long-term global offtake contracts. |

+-----------------------------------------------------------------------+

1. The Byproduct Capture Function

Critical minerals rarely appear in high-grade standalone economic deposits. Instead, they are recovered as minor byproducts during the industrial-scale refining of base metals. Gallium, for example, is primarily recovered during the processing of bauxite into aluminum. Because China maintains the world's largest aluminum smelting infrastructure, it captures gallium as a low-cost structural externality. A country without an active, large-scale aluminum smelting ecosystem cannot spin up a domestic gallium extraction supply chain overnight, regardless of capital injection, because the underlying base-metal throughput does not exist.

2. The Midstream Processing Monopoly

The primary point of vulnerability for Western supply chains is not resource extraction (upstream mining), but chemical refinement (midstream processing). Converting raw, toxic ore or industrial byproducts into 99.999% pure electronic-grade material requires substantial capital expenditure, long regulatory runway times, and high tolerances for localized environmental degradation. For instance, Chinese dominance in germanium refining stems from processing coal fly ash—a hazardous byproduct of coal-fired power plants that carries significant air quality and waste management liabilities that are strictly regulated or prohibited in Western jurisdictions.

3. Preventative Offshore Asset Acquisition

Where domestic geology is insufficient, Chinese enterprises utilize state-backed capital to execute aggressive overseas acquisition strategies, effectively pricing out Western private equity firms bound by traditional internal rate of return (IRR) metrics.

A clear example of this mechanism occurred during the consolidation of the Ngualla rare earth deposit in Tanzania. Originally discovered by an Australian firm with intentions to establish an integrated supply chain routed through the United Kingdom, control of the asset shifted permanently when Shenghe Resources, via its subsidiary Ganzhou Chenguang Rare Earths New Material, acquired the asset for approximately AU$158 million. Despite a subsequent, structurally higher non-binding counter-offer from a Western private equity group backed by strategic defense advisers, the institutional velocity and capital premiums offered by the state-supported entity secured the asset. By 2029, current offtake agreements dictate that 100 percent of rare earth production from this premier emerging deposit will flow directly to Chinese refiners.

The Strategic Failure of Western Countermeasures

Western efforts to decouple their technology supply chains from this bottleneck have relied on traditional market mechanisms and regulatory frameworks that fail to account for the structural economics of the minerals sector.

The Limitations of Ramping Extraction

The prevailing policy response in the United States and the European Union emphasizes the expansion of domestic mining permits. This approach suffers from three systemic flaws:

- The Valuation Mismatch: Upstream mining assets operate on volatile commodity cycles, making them poorly suited for the consistent, low-margin returns required by traditional public equity markets.

- The Refining Bottleneck: Extracting ore domestically without domestic refining capacity forces Western operators to export raw concentrates directly back to Chinese facilities for chemical purification. This preserves the exact geopolitical leverage it intends to break.

- The Valley of Death for Technology Scaling: Early-to-growth stage mining technology companies struggle to bridge the gap between bench-scale chemical proofs and industrial-scale deployment. Federal funding mechanisms are routinely optimized for established Base-Metal conglomerates rather than agile metallurgy innovators.

Operational Mitigations and the Leapfrog Vector

Because the United States and its allies cannot out-mine or out-process highly subsidized state systems within a relevant strategic timeframe, strategic planning must shift from replication to structural leapfrogging.

1. Scaling Automated Discovery and Process Optimization

Deploying machine learning models to analyze hyperspectral remote sensing data and seismic records dramatically shortens exploration timelines. Instead of relying on decade-long geological mapping cycles, predictive algorithms can target high-probability deposits containing secondary critical mineral concentrations within existing, operational domestic waste streams.

2. Capitalizing on Industrial Waste Metallurgy

Rather than opening new open-pit mines, industrial policy must prioritize the extraction of elements like gallium, germanium, and cobalt from historical industrial waste, such as:

- Tailings ponds from abandoned mining operations.

- Coal fly ash repositories.

- Electronic waste (e-waste) processing facilities.

Developing high-yield, closed-loop chemical recycling protocols allows advanced economies to bypass the upstream mining phase entirely, securing high-purity inputs at a lower thermal and environmental cost per kilogram.

3. Alternative Material Science Deployment

To permanently break the midstream dependency, hardware design must pivot toward material substitution. This requires active funding for solid-state physics research into alternative substrates that minimize or eliminate the use of restricted REEs in high-efficiency cooling motors and power delivery networks.

Strategic Playbook for Technology Enterprises

Technology firms and infrastructure operators can no longer treat hardware supply chains as outsourced procurement problems. To protect computational sovereignty, organizations must execute three immediate operational shifts:

- Enforce Material Provenance Mandates: Establish strict cryptographic tracking for all tier-three and tier-four hardware components, ensuring that semiconductor inputs are sourced from verified, non-monopolized supply chains.

- Participate in Direct Physical Offtake Offsets: Large technology consortia must pool capital to issue long-term, guaranteed purchase contracts for domestic and allied midstream processors, shielding these critical refiners from the predatory pricing strategies frequently deployed to suppress Western market entry.

- Design for Material Elasticity: Engineering teams must build modular hardware architectures capable of swapping component specifications based on raw material availability, preventing single-source mineral shocks from shutting down entire server infrastructure deployments.